Banking ecosystem of India has seen unprecedented changes in terms of delivery and product in the last few years. It has moved from a traditional product centric, inside-out approach, to a consumption based, outside-in approach. Pioneered by BFSI players like Yes Bank, Kotak bank, DCB bank, etc., the Open Banking ecosystem has now grown to include NBFC and other tech players who have created partnerships within the system. Open Banking has now become a part of the Indian financial services and fintech segment.

Unlike the Open Banking initiatives seen in countries like the UK and US, which are either completely market driven or regulations driven, India has adopted a hybrid model where both the market and government take active roles in the ecosystem's development. In 2016, India launched Unified Payment Interface (UPI), allowing an individual to access his bank accounts from registered apps (such as Google Pay) and make transactions to any other bank. With such major initiatives being brought to the market by the National Payments Council of India (NPCI), the BFSI sector is evolving into an APIbased collaborative model. Additionally, the emergence of players like Neo Banks, Digital Banks & API Aggregators are simplifying life for customers and creating new business models. Recently, larger players like ICICI have also joined the game through the release of their developer portal which consists of over 250 APIs.

Embedding of banking services on SaaS (Software-as-a-Service) based accounting platform is a classic use case of Open Banking. This allows SMEs/MSMEs to fulfil their core need of managing customer receivables and payable on their accounts and also allows them to make payments to partners and collect money from customers.

Business case of Open Banking in India

Traditionally, bankers have taken an inside-out approach to business and have designed products and services for customers based on internal discussions. Here, the innovations were driven by keeping the products of the bank in mind and with little regard to the customer’s needs. In contrast, Open Banking has affected the banking perspective by adopting an outside-in approach where banks work with their partners, on a revenue sharing model, to provide the best solutions to customers. Banks leverage their APIs, Capital, and customer loyalty to partner with fintech players who are agile and have a strong technology background to create innovative products and ease the customer journey. Taking this a step further, banks are now building custom platforms to fulfil specific needs of corporate customers. While the traditional banking mindset has been the foundation of banking, Open Banking has provided new perspectives to make banking easier, efficient, and customer friendly.

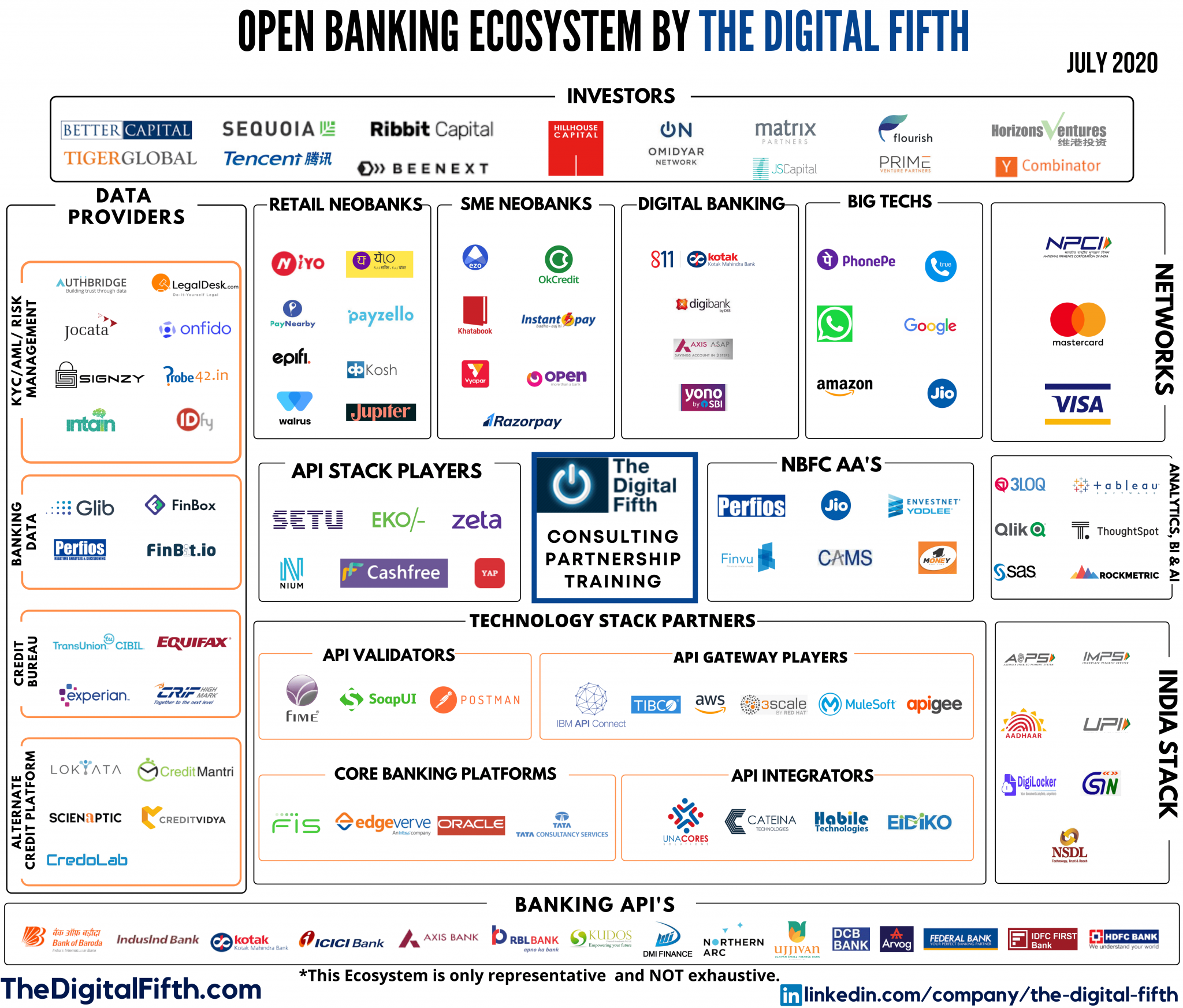

Open Banking ecosystem of India

The Indian Open Banking network can be broadly classified into five categories.Banks and NBFCs, form the bottom layer of the ecosystem and offer their APIs to perform services like Payments, Lending and Collections. This Layer is powered by technology stack partners and supported by an emerging breed of API Integrators which have the coding expertise necessary. The requests sent to these banking APIs are further filtered by the API Gateway players such as IBM or Redhat, who provide an additional level of security to the Bank APIs. This ecosystem is enabled by key players who perform tasks like data validation and analytics. The next layers within the ecosystem consist of enablers powering new solutions around Open Banking. Open Banking cannot be truly achieved without the democratisation of the customers’ financial data. With the RBI’s directive giving customers the control to share their financial data via NBFC AAs, they enable customers to view all their financial information in a single platform and allow consent-based sharing with third parties. The effectiveness of this network has led to the rise of several use cases like neobanks, digital banks, and big tech players who use bank APIs for their underlying operations and provide highly specialised services to solve the specific pain-points of their respective segments. The ecosystem is also supported by investors.

Click on the picture for the enlarged version

Conclusion

With the entry of Account Aggregators and the establishment of newly formed setup for Lending, OCEN (Open Credit Enablement Network) the ecosystem is poised for the next phase of growth, not only from the banking ecosystem but also from sectors like insurance and securities. This has led to an increase in the number of use cases. On the other hand, due to the unprecedented growth in this sector, a larger segment of investors is now focused on fintech players who work in the Open Banking space.

The editorial was originally published in Global Open Banking Report 2020, which follows the journey from Open Banking to Open Finance and Open Data Economy and provides key insights about the benefits of Open Finance for different areas of financial service.

About Sameer Singh Jaini

Founder and CEO of The Digital Fifth, Sameer has over 2 decades of experience in Digital Banking, Open Banking, and Fintech.

About Shashank Shekhar

Shashank is Head of Consulting at The Digital Fifth and has experience in technology infrastructure, Digital banking, Open Banking, and governance.

About The Digital Fifth

The Digital Fifth is India’s first fintech consulting and advisory firm for banks and financial institutions. We have been the go-to solution finders for established BFSI organisations and emerging fintech players alike, where we focus on adding value to our client’s businesses and help them create an impact. We also provide digital and fintech training across segments; and leading connect in India for international fintech hubs and startups.